The “New Irvine” Entry Strategy: Moving Beyond the Median

Buying your first home in Irvine, California, is one of the most exciting—and most complex—real estate decisions you will ever make. You are not just buying a property; you are choosing a school district, a village, an HOA, a tax structure, and a community lifestyle, often all at once.

The mistake most buyers make is looking at the “Irvine Median” and walking away. As of early 2026, the median home price in Irvine hovers around $1.5M–$1.6M. To a first-time buyer, that number can feel disqualifying. But it doesn’t tell the full story.

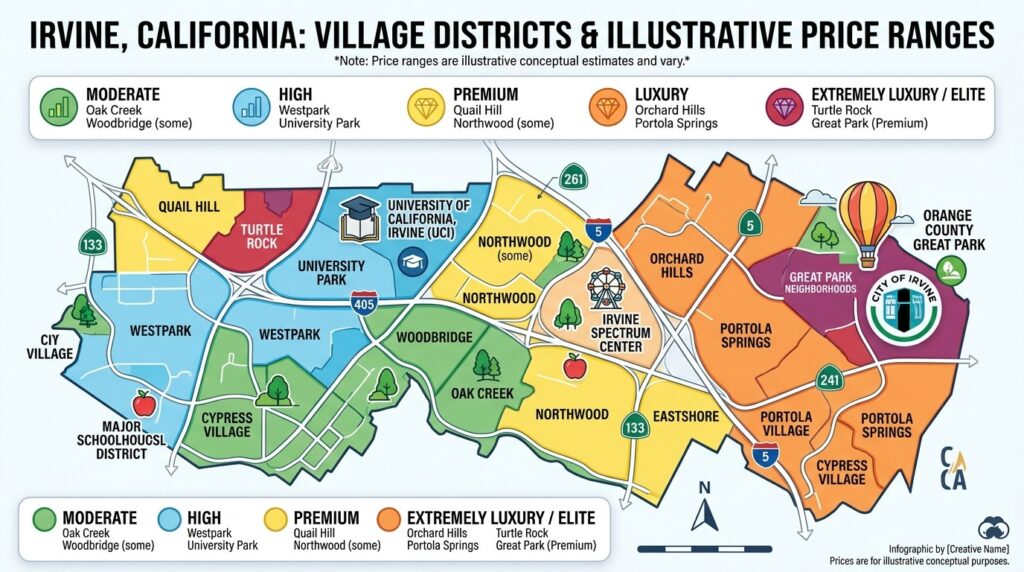

Irvine is not one market. It is 35+ distinct villages, each with its own pricing, HOA fees, Mello-Roos tax levels, and buyer competition. This guide is built to help you navigate that complexity with the clinical precision of a professional advisory briefing.

Part 1: The First-Timer’s Foothold — The Attached Home Market

While the $1.6M single-family home may be the Irvine headline, the attached home market (condos and townhomes) is where the real activity is for first-time buyers.

- Entry Points: First-time buyers can enter the Irvine market at price points ranging from $650,000 to $1.1M depending on the village and unit size.

- Market Momentum: Sales of attached homes in Irvine jumped over 40% year-over-year in 2025, signaling a massive shift toward this segment by first-time buyers.

- Strategy: The key is knowing which village offers the “Sweet Spot”—the best balance of modern construction, manageable taxes, and price appreciation.

Part 2: The Budget Conversation Nobody Has With You

In Irvine, your true monthly housing cost is almost never just your mortgage payment. This is where buyers get blindsided.

The Four Layers of Irvine Housing Costs

- Mortgage Principal & Interest: Your base loan payment.

- Property Taxes: A base rate of 1.1%, subject to Prop 13.

- HOA Dues: Typically $200–$600/month in most Irvine villages. These cover the resort-style pools, parks, and trails Irvine is famous for.

- Mello-Roos Special Assessments: This is the “hidden” variable.

The Mello-Roos Moat

Mello-Roos is a special tax used to fund infrastructure in newer communities.

- In newer villages like Portola Springs or Great Park, Mello-Roos can add $2,000 to $8,000+ annually to your tax bill.

- In older villages like Woodbridge or Northwood, Mello-Roos is often minimal or non-existent.

- The Impact: For a first-time buyer, this distinction can change your monthly cost by $200 to $600 per month.

Part 3: The 2026 Village-by-Village Breakdown

Where you buy determines how you live and what you pay. Here are the top village recommendations for the first-time buyer profile.

1.

Woodbridge: The Entry-Point Classic

- Why it wins: Developed in the 70s/80s, it offers mature trees, two man-made lakes, and a resort feel.

- Tax Advantage: It has some of the lowest Mello-Roos exposure in the city.

- Price Range: Condos and townhomes typically start around $750K–$950K.

2.

Northwood: The Family-First Suburb

- Why it wins: Classic suburban experience with tree-lined streets and high-performing schools.

- Budget: Attached homes range from $800K–$1.1M with minimal Mello-Roos.

3.

Portola Springs: Modern Luxury (With a Cost)

- Why it wins: Modern architecture and brand-new community parks.

- The Trade-off: Mello-Roos here can exceed $5,000/year. It is a critical variable to model before falling in love with a listing.

4.

Cypress Village: The “Sweet Spot” Value Play

- Why it wins: Newer construction at slightly lower price points than Great Park or Orchard Hills. It offers a high-end feel for those who want modern amenities without the $2M price tag.

Part 4: Financial Engineering — CalHFA in Irvine

Most buyers assume assistance programs like CalHFA don’t work in Irvine. This is a costly assumption.

- Attached Home Opportunity: While CalHFA isn’t meant for $2M estates, it is perfectly suited for the $700K–$850K condo market in Woodbridge or Northwood.

- Down Payment Help: The “MyHome Assistance” program can provide a junior loan for up to 3.5% of the purchase price. On an $800,000 condo, that is $28,000 in capital you don’t have to provide upfront.

- Strategy: Combine CalHFA with a low Mello-Roos village to maximize your qualifying power.

Part 5: How to Win — The Offer Strategy

Irvine is competitive. To win as a first-timer, you must act with the sophistication of an institutional investor.

- Underwritten Pre-Approval: Don’t just get a “pre-qual” letter. Get fully underwritten. Listing agents in Irvine take this as a sign of financial certainty.

- Mello-Roos Archaeology: Always request the CFD (Community Facilities District) disclosure before writing an offer.

- Target “Aged” Inventory: Look for homes with 30+ days on the market. These sellers are more likely to negotiate on price or closing costs.

- The Agent Network: Many of the best deals in Irvine happen “off-market” through agent-to-agent relationships. Your choice of representative is your greatest asset.

FAQ — First-Time Home Buyer Irvine CA

- Q: What is the minimum down payment?

- Conventional and FHA loans allow for 3% to 3.5% down. On a $900K property, that’s roughly $45,000.

- Q: Which village is “best” for my budget?

- Woodbridge and University Park offer the lowest taxes; Cypress Village offers the best modern value.

- Q: How competitive is the market in 2026?

- The under-$1M segment is very competitive, with well-priced homes often receiving multiple offers within 7 to 10 days.